Capital or pension: The security aspect - longevity risk

Flash #6, November 14, 2024

In Economico Flash 4, we have provided an overview of the “capital versus pension” decision. In Flashes 6 & 7, we look at the security aspect.

As we know, many things can go wrong in life. If you draw a lump sum instead of a pension when you retire, two things come into play: firstly, you can live longer than average – which is actually a good thing – but the lump sum will then run out (longevity risk). Secondly, you can lose the capital you have withdrawn either on the stock market (capital market risk) or for other reasons.

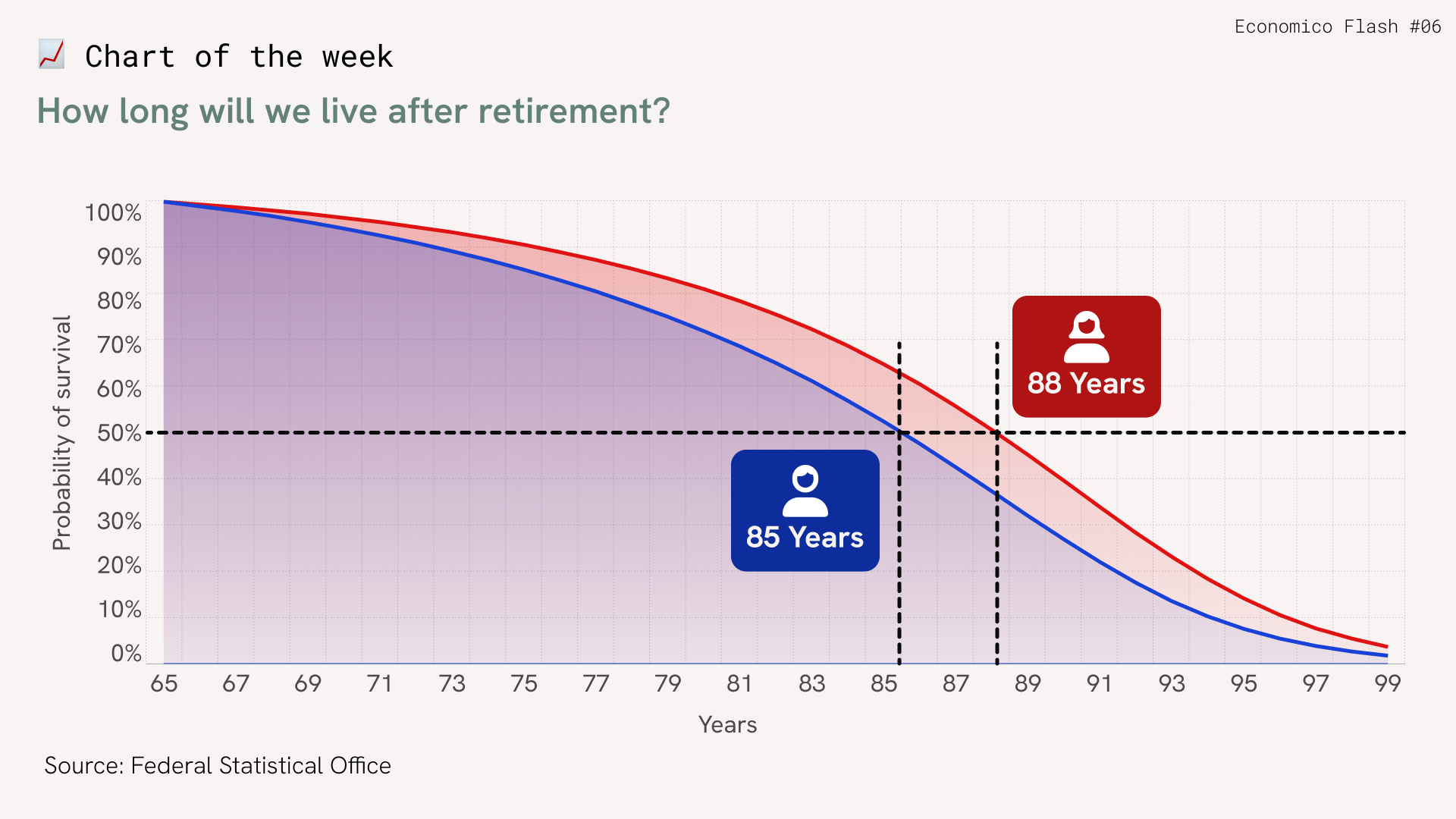

In this Flash, we deal with longevity risk. Although people do not like to calculate their own demise, we unfortunately have to make an exception today. So if you live longer than average after retirement (: 85y / : 88y), there is a risk that you will run out of money if you withdraw your capital. The probability that you will live longer than the average is 50 percent. The probability that you as a woman will reach the age of 90 is 40 percent, and the probability of reaching the age of 95 is 14 percent. In any case, these probabilities are much higher than winning a significant prize in the lottery or any other game of chance.

Are you financially secure if you are lucky enough to reach old age? You do not need to worry if you draw a pension, as you can rely on a steady income even in old age. The old-age pension for you and your entitled partner(s) will be paid for life.

The situation is different in the case of a lump-sum withdrawal. Of course, if you have additional funds saved for rainy days or are thrifty and can manage with the AHV pension, the lack of pension income will not cause you any stomach ache.

However, if you finance part of your consumption in old age by using up the capital you have withdrawn, you could face the horror scenario of personal bankruptcy or having to rely on state supplementary benefits in the event of longevity. This comes at a time when you typically have other worries.

If you want to avoid the longevity risk and sleep soundly in old age, we recommend an annuity.

Takeaways

- With a lump-sum withdrawal, you expose yourself to longevity risk.

- The longevity risk is relevant for you if you are dependent on the capital from the 2nd pillar to finance your consumption in old age.

Takeaways

- With a lump-sum withdrawal, you expose yourself to longevity risk.

- The longevity risk is relevant for you if you are dependent on the capital from the 2nd pillar to finance your consumption in old age.