Capital or pension: comparison of returns

Flash #5, November 7, 2024

In Economico Flash 4, we provided an overview of the “capital or pension” decision. In this Flash 5, we focus on the return aspect.

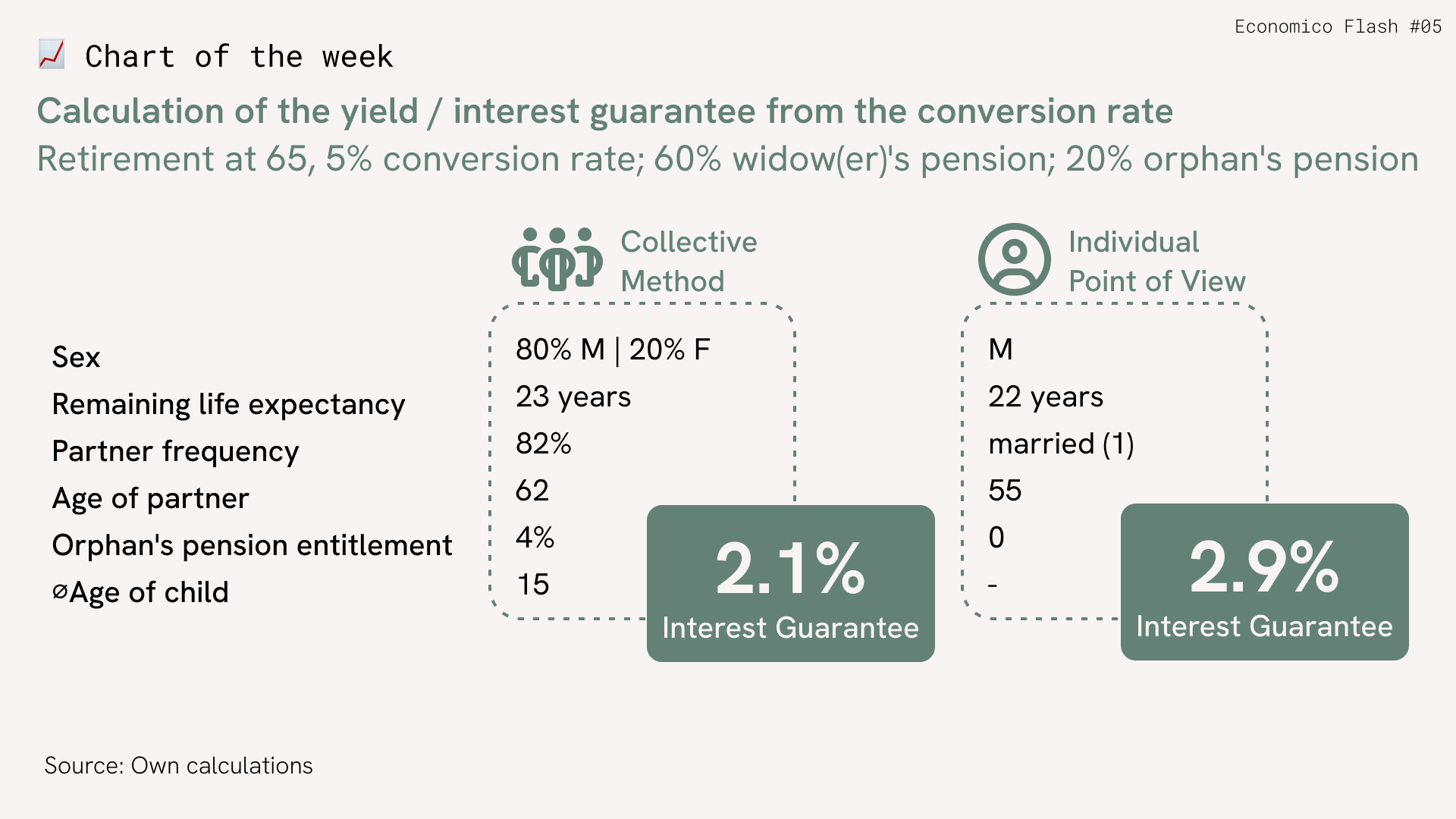

The return on the pension can be implicitly derived from the level of the conversion rate (UWS). Its calculation is based on the consideration of how much return the pension fund must generate annually on the retirement assets available at the time of retirement in order to finance the pension payments until the (on average expected) end of your life and the survivors who are also insured through the retirement pension. This calculation is based on the general principles of life expectancy. Some people die a little earlier, others live a little longer, but on average the calculation works out for the pension fund, which has a large number of insured persons. Using this collective calculation method, it can be calculated that the return or interest guarantee at a conversion rate of 5.0% corresponds to around 2.1%.

Of course, your individual life expectancy and situation may not correspond to that of the average person. From an individual point of view, the implicit return on a conversion rate also changes. It increases with longer life expectancy, and it also increases if you live with a younger partner who is entitled to benefits in the event of your death. And vice versa. Your decision is based on your individual situation and not that of the average person.

Finally, it should be noted that the interest guarantee on the pension is a minimum benefit that can be adjusted upwards by your pension fund through pension bonuses and, if inflation continues, through inflation adjustments.

In Economico, we currently provide you with the calculation of the interest guarantee resulting from the conversion rate of your pension fund using the collective method. A calculation function for the individual calculation is being planned.

If you now decide on the capital, you should achieve a net return after costs that at least corresponds to the interest guarantee from the pension. With average asset management costs of 1.37% (according to Economico Flash 1), this requires a gross return before costs of around 3.5%. To achieve this return, an investment strategy with a substantial equity component is required. Such an investment strategy is associated with risks of loss, which we discuss in Flash 7 after next.

Takeaways

- Collective: 5% UWS ⇔ approx. 2.1% interest guarantee

- Your individual situation has an influence on the amount of the interest guarantee on pension withdrawal

- Do you achieve a net return > interest guarantee on the lump-sum withdrawal?

Takeaways

- Collective: 5% UWS ⇔ approx. 2.1% interest guarantee

- Your individual situation has an influence on the amount of the interest guarantee on pension withdrawal

- Do you achieve a net return > interest guarantee on the lump-sum withdrawal?