Legal Planning: The Beneficiary Designation (in the 2nd and 3rd Pillars)

Flash #66, June 4, 2026

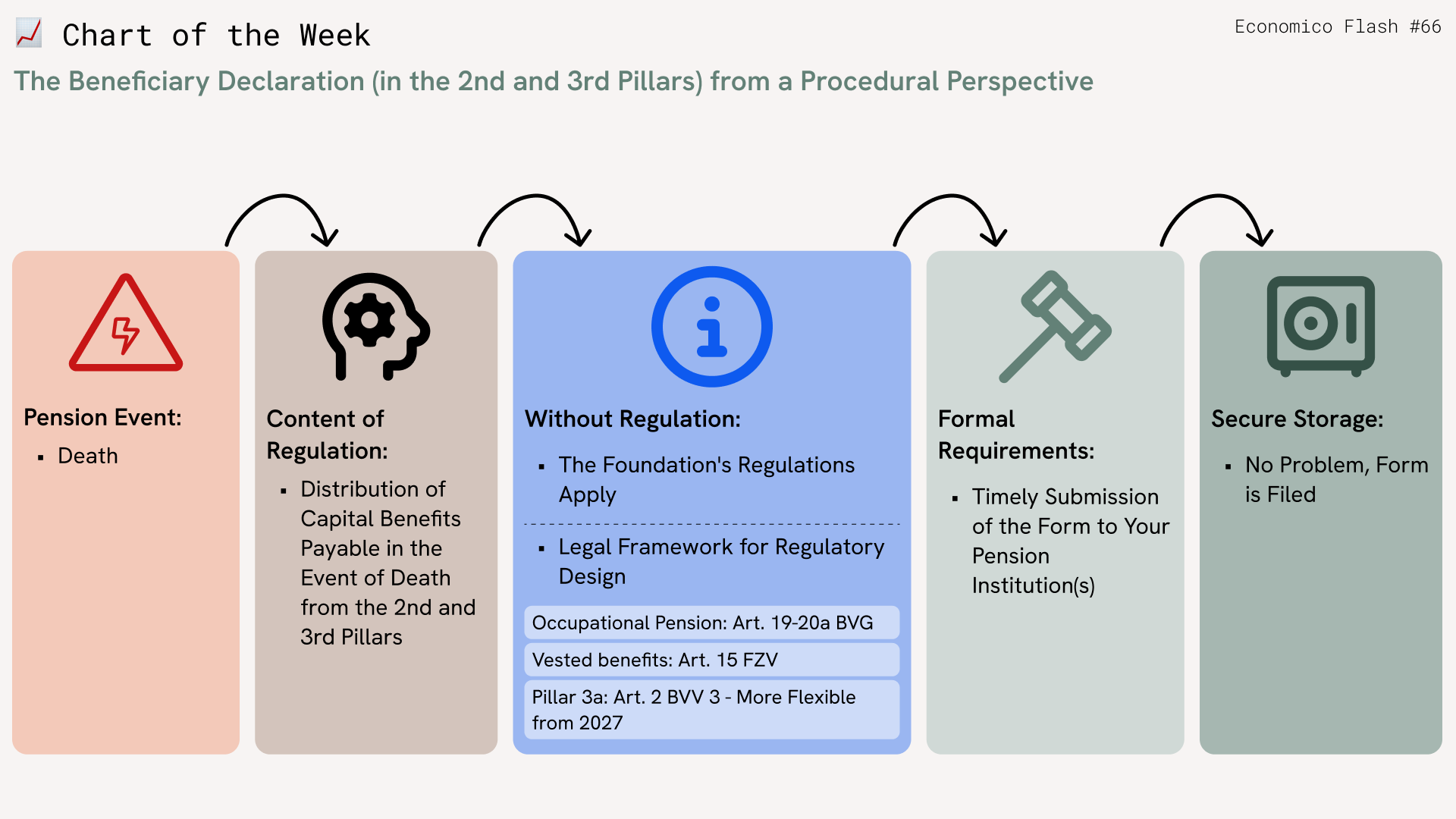

Triggering Event:

The beneficiary designation(s) in the 2nd and 3rd pillars take effect in the event of death.

Content of the provision:

With the beneficiary designation, you determine the distribution of lump-sum benefits from the 2nd and 3rd pillars due upon death to your surviving dependents. However, widow’s/widower’s pensions and orphan’s pensions from your pension fund cannot be individually designated, as they can only be paid to beneficiaries defined by law. And importantly: The beneficiary declaration must be submitted or filed separately with each 2nd and 3rd pillar pension fund. The scope for customization depends on the law and the pension fund’s regulations. Speaking of the law: In occupational pension plans, pension funds already enjoy considerable flexibility in the regulatory design of beneficiary provisions. This is not the case in the third pillar: Until now, rigid distribution rules have applied to the distribution of assets accumulated in pillar 3a in the event of death. However, as of January 1, 2027, a legislative amendment will take effect that also allows for flexible structuring of beneficiary provisions in pillar 3a.

What happens without a provision:

If you do not submit a beneficiary designation, the pension fund’s regulations will apply. If the pension fund does not include a provision in its regulations, the law applies: In occupational pension plans, the “statutory fallback” is found in Art. 19 and 20 BVG; Art. 20a BVG grants pension funds under the BVG the discretion to structure their regulations.

If you have assets with a vested benefits institution, Art. 15 FZV serves as the legal basis for beneficiary designation.

Finally, Art. 2 BVV 3 provides the legal framework for the distribution of accumulated 3a assets. As a rule of thumb: Assets accumulated in the 3rd pillar and in vested benefits are always distributed, whereas death benefits from occupational pension plans are distributed only if, in the event of death, the beneficiaries designated by law and the regulations exist.

Formal requirements and retention:

For your beneficiary designation to be legally effective, you must submit it to and file it with your pension fund. Typically, pension funds provide standardized forms for this purpose on their websites. And as a reminder: The beneficiary designation must be completed and submitted separately for each pension fund.

Takeaways

- Beneficiary designations allow you to specify how capital benefits from the 2nd and 3rd pillars are to be distributed in the event of death

- One beneficiary designation per pension fund

Takeaways

- Beneficiary designations allow you to specify how capital benefits from the 2nd and 3rd pillars are to be distributed in the event of death

- One beneficiary designation per pension fund