Capital or Pension: Overview

Flash #4, October 31, 2024

If you draw a pension from your pension fund, you can sleep soundly in old age. This perhaps somewhat bold principle can certainly be taken to heart in the “capital versus pension” decision.

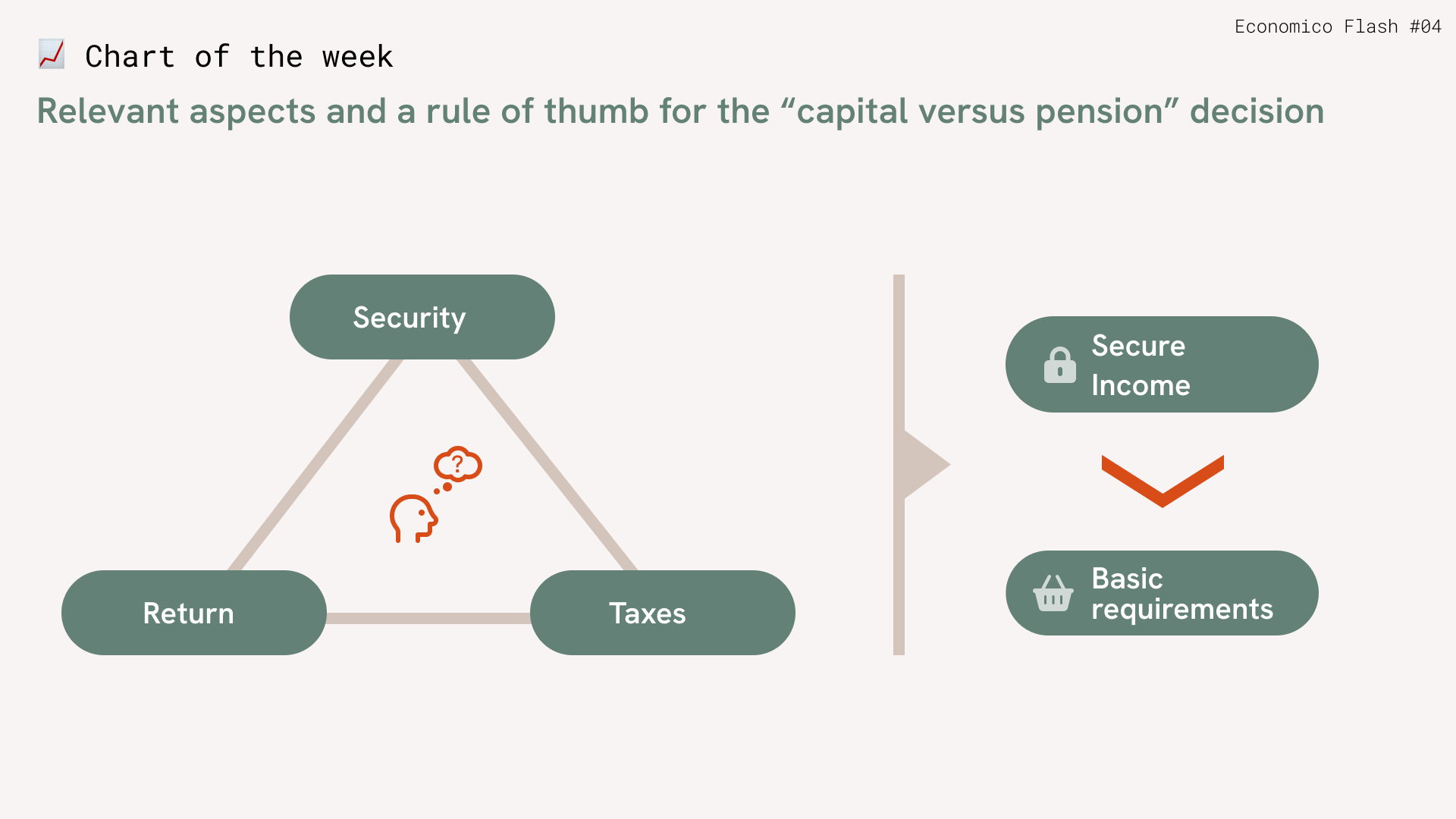

The full range of arguments for this undoubtedly important and groundbreaking decision can be boiled down to the three decision dimensions of security, returns and taxes, which we will examine individually in the three upcoming Economico Flashes. Below we present an overview of the three aspects and a simple rule of thumb for weighing them up.

Return: The conversion rate is the percentage rate at which the retirement assets are converted into a lifelong pension at the time of retirement. The standard conversion rate of 5% results in a lifelong interest or return guarantee of at least 2%. This return must first be earned on a lump-sum withdrawal – nota bene net of costs. More on this in Economico Flash 5.

Security: A lot of unforeseen things can always happen in life, but with a lump-sum withdrawal you take on the two additional risks of longevity risk (more on this in Flash 6) and capital market risk (more on this in Flash 7) compared to a pension.

Taxes: The lump-sum withdrawal is subject to (lower) capital gains tax, while the annual pension is subject to (higher) income tax.

This simple comparison implies the well-known tax advantage of capital withdrawal. More on this in Economico Flash 8.

The three decision dimensions are fundamentally in conflict with each other. Your personal preferences are ultimately decisive for the resulting weighing up of interests. However, as a practical rule of thumb, it makes sense to draw at least enough pension from the pension fund, together with other secure sources of income (AHV income, rental income from property, etc.), to at least cover your basic needs in old age. This way you can sleep soundly in old age.

Economico provides you with a powerful analysis function to evaluate the various dimensions of the “capital versus pension” decision tailored to your individual starting position.

Takeaways

- Capital versus pension: Safety first!

- Security, return and tax considerations require an individual weighing up of interests

- Basic needs in old age should be covered by a secure income.

Takeaways

- Capital versus pension: Safety first!

- Security, return and tax considerations require an individual weighing up of interests

- Basic needs in old age should be covered by a secure income.