3a & Vested Benefits: Insurance Solution

Flash #59, January 29, 2026

The track record of insurance solutions in the 3rd pillar and in vested benefits is — there is unfortunately no other way to put it — dismal. It is therefore hardly surprising that this product segment has not only consumer protection authorities, but also the financial market supervisory authority breathing down its neck. Equally unsurprising is the fact that — as already outlined in Flash 57 — insurance solutions in pillar 3a and vested benefits are increasingly losing market share.

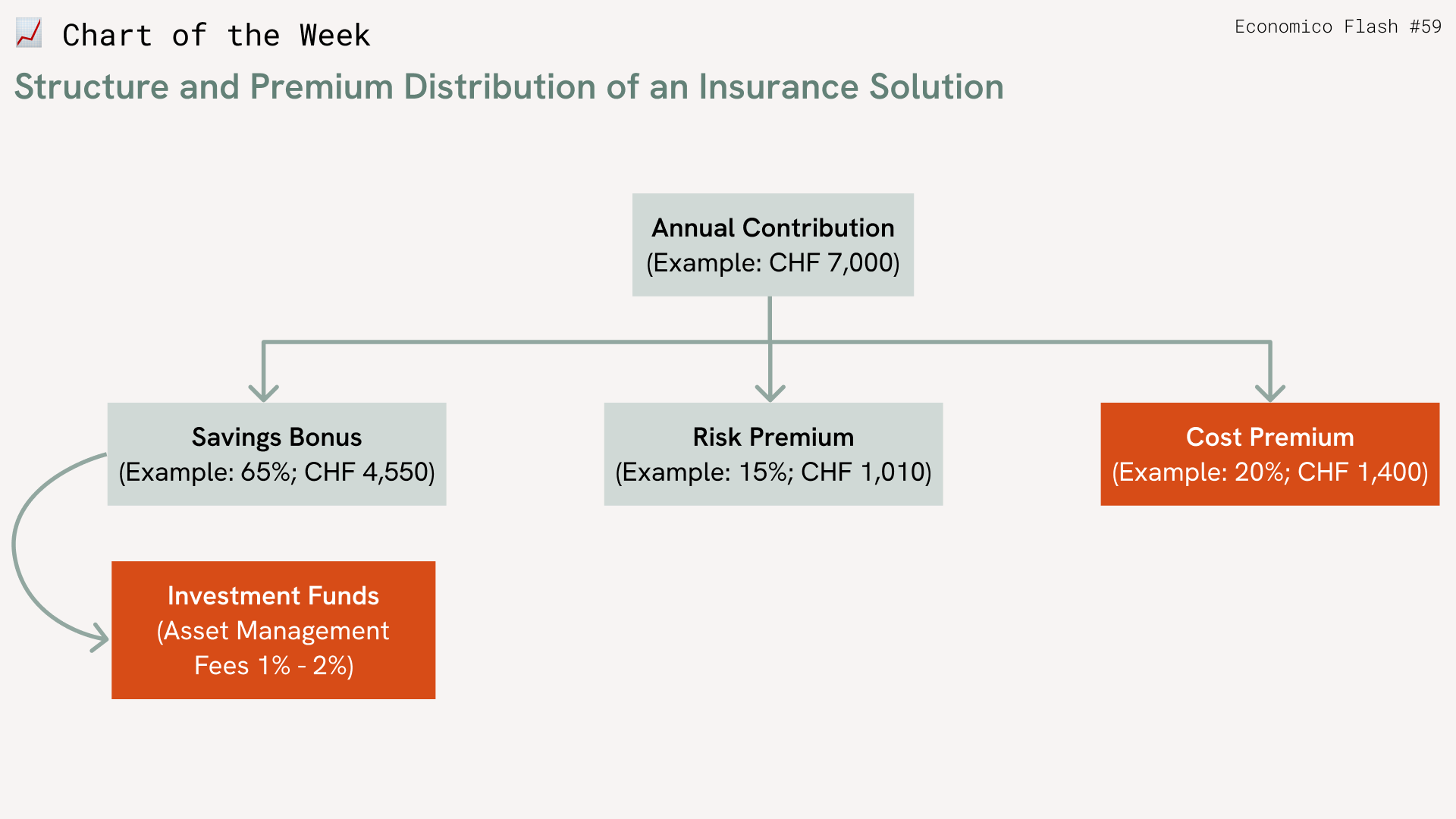

Let us take the trouble to examine the basic mechanics of a unit-linked insurance policy a little more closely. Such policies are commonly offered on the market as insurance solutions within the 3rd pillar or as part of vested benefits solutions. The amount paid in annually is — as illustrated in the Chart of the Week — split into three components: savings premium, risk premium, and cost premium.

The savings premium flows into an investment product, which in turn generates additional costs. These costs — even when considered in isolation — are significantly higher than the asset management costs of a competitive securities-based solution.

The risk premium finances the event covered by the insurance policy — typically death, disability, or unemployment. This premium is also calculated in such a way that the insurer is certain not to make a loss on this part of the business.

The cost premium, on the other hand, is simply a cost block with no direct benefit in return. The corresponding portion is retained by the insurer.

The example figures shown in the Chart of the Week are derived from a typical insurance solution structure: one portion of the premium is invested as a savings component, another portion serves as risk coverage, and a significant share goes towards costs.

A 3a or vested benefits insurance solution is also typically taken out with very long terms of up to 30 years. This means that policyholders are bound by the contractual terms for the entire duration of the contract and must meet their annual contribution obligations. Should an early exit from the contract occur, this will in many cases result in considerable losses in value.

Unit-linked insurance policies are therefore a prime example of financial products that investors would be better off avoiding. The bundling of various product components leads to a lack of transparency — and a lack of transparency frequently results in excessive costs.

Those who wish to invest and hedge against certain risks at the same time are generally better served by a separate approach: first define a suitable investment strategy and transparently compare providers of securities-based solutions. Then — if desired — separately select an insurance solution for specific risks and compare those competitively as well.

Takeaways

- Insurance solutions are opaque and (too) expensive.

- Once again: only buy what you understand!

Takeaways

- Insurance solutions are opaque and (too) expensive.

- Once again: only buy what you understand!