Tax implications of a buy-in(to the 2nd or 3rd pillar)

Flash #42, September 4, 2025

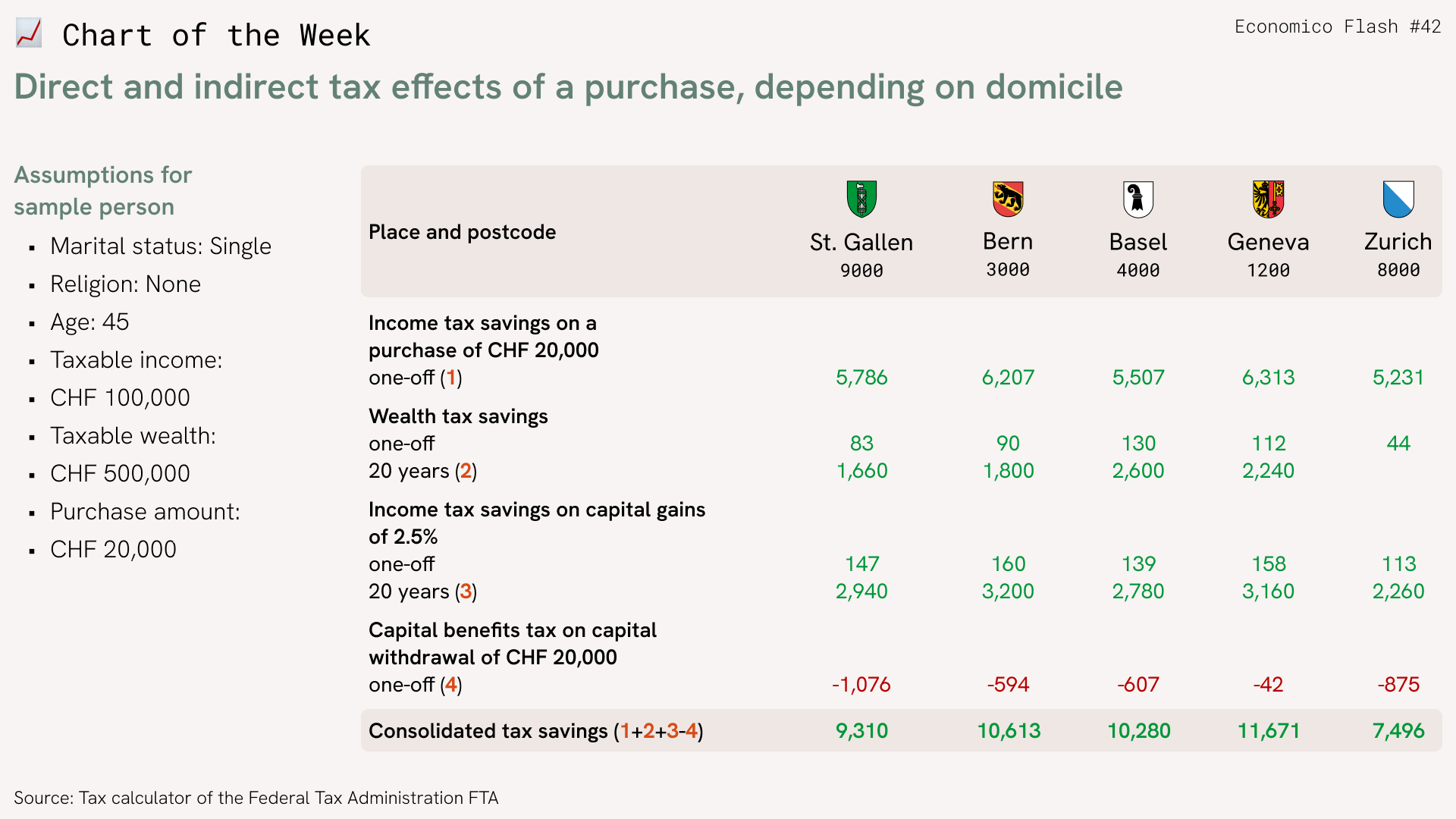

Buying into the second pillar or pillar 3a is usually motivated by a tax advantage. This advantage does indeed exist – and it is even greater than one might think. The reason lies in indirect tax effects that are often overlooked in many analyses.

Let us consider a representative example: a 45-year-old with a taxable income of CHF 100,000 per year and taxable assets of CHF 500,000. This person is considering paying CHF 20,000 into their pension fund and having this capital paid out as a lump sum upon retirement at age 65. What direct and indirect tax effects does this generate?

- In the year of the buy-in, taxable income is reduced from CHF 100,000 to CHF 80,000. Depending on your tax domicile, this allows you to save on income taxes.

- At the same time, the buy-in also reduces taxable assets by CHF 20,000. This tax saving may seem small at first glance, but it applies not only in the year of the contribution, but also in every subsequent year until retirement. Over the years, this can add up to substantial savings in wealth tax.

- The capital continues to work and generates returns. In Flash #11, we showed that annual interest credits of 2% or more on pension fund assets have been in line with market conditions in recent years. No income tax is levied on this interest. Without a buy-in, achieving a comparable net return would require holding a balanced portfolio of roughly 50% equities and 50% bonds. Over the past ten years, however, such a portfolio generated around 2.5% in taxable investment income per year – about CHF 500 on CHF 20,000, which would have to be taxed as income each year.

- Upon retirement and withdrawal of the CHF 20,000 in capital, a one-off capital withdrawal tax is due.

The Chart of the Week presents a simple model calculation for various tax domiciles, combining these four tax effects into a net tax effect.

Takeaways

- Making a buy-in to the 2nd or 3rd pillar is a good idea from a tax perspective.

- Due to indirect tax effects, the tax benefit of a buy-in is actually greater than one might think.

Takeaways

- Making a buy-in to the 2nd or 3rd pillar is a good idea from a tax perspective.

- Due to indirect tax effects, the tax benefit of a buy-in is actually greater than one might think.